In the early 2000s, if someone had said that in the near future almost every automobile would operate through mobile applications, could be charged at home instead of refueled at a gas station, and would be connected to the internet, most people would probably have smiled dismissively.

Today, however, we are right in the middle of a much larger transformation in the automotive sector. For years, whenever automotive professionals gathered and the discussion turned to electric vehicles, we talked about “range anxiety,” battery capacity, charging duration, and battery-related concerns. But as of 2026, the real question has changed.

Can the world truly manage such a rapidly expanding charging infrastructure in a secure and sustainable way?

According to the Turkish Energy Market Regulatory Authority (EPDK) February 2026 statistics, the number of electric vehicles on Turkish roads reached 399,043, while the number of public charging sockets exceeded 40,575. In the same month, total electricity consumption at charging stations was recorded at 53.4 million kWh. By March 2026, the number of charging sockets increased to 41,938, with total installed capacity reaching approximately 3,190 MW.

Istanbul alone accounted for nearly one-third of the country’s total charging consumption in February.

Looking ahead to 2030, the picture becomes even more striking: the number of electric vehicles on Turkish roads is expected to reach between 1 and 1.5 million — nearly four times today’s figures.

Interestingly, this number was only around 15,000 in 2022.

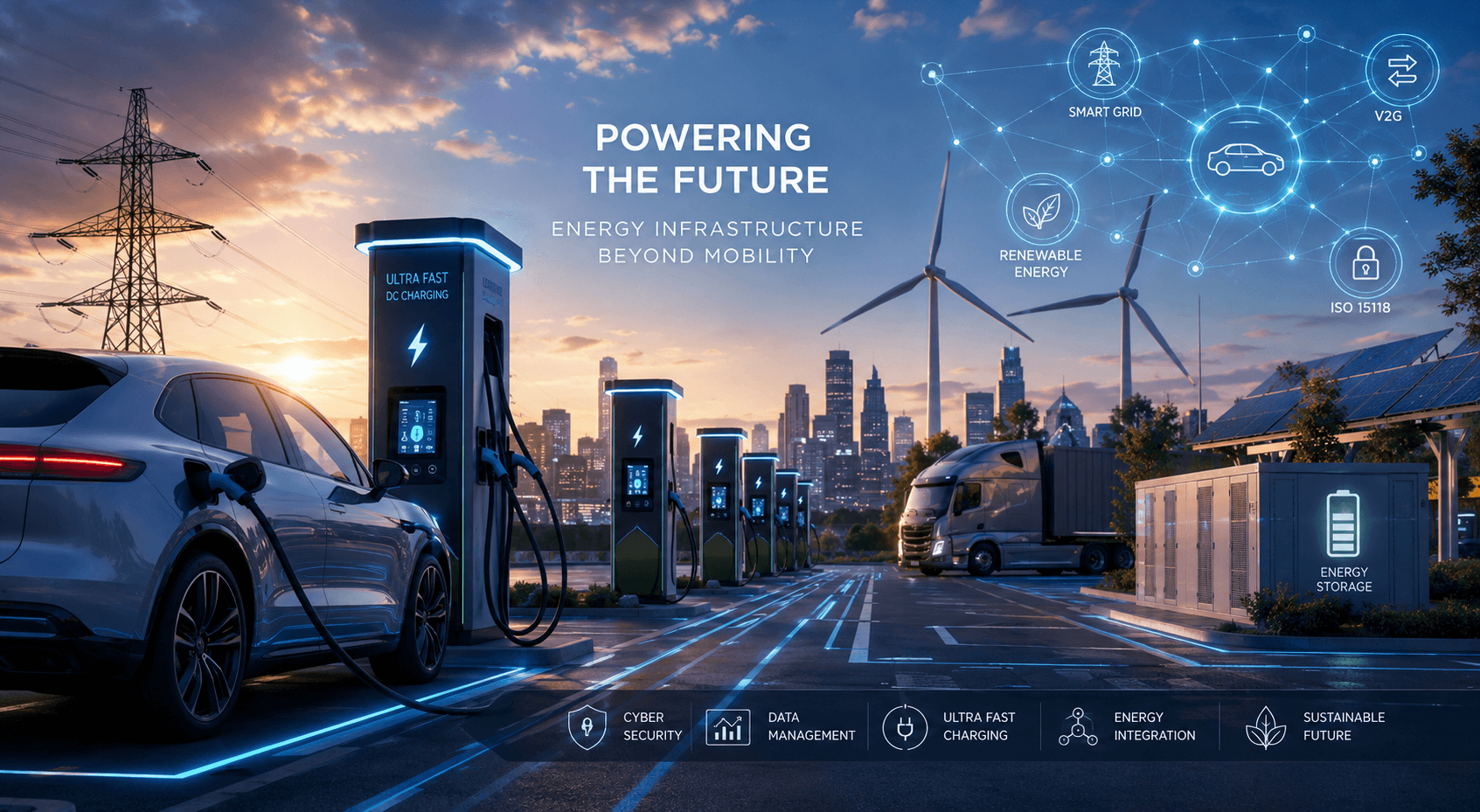

Türkiye is now among the countries entering a phase of rapid growth in this field. Yet the real turning point lies elsewhere. You may already have heard of the Megawatt Charging System (MCS) standard developed in Europe for heavy commercial vehicles. In short, long-haul transportation is also entering the electrification era in Türkiye. This means charging infrastructure is no longer merely an automotive-sector issue. Today, an ultra-fast charging hub can consume nearly as much energy as a small industrial facility.

On the European Union side, the AFIR update, which entered into force on 8 January 2026, made ISO 15118 support mandatory for all newly installed public AC charging points. From 2027 onward, the ISO 15118-20 standard — including Plug & Charge technology, where the vehicle and charger authenticate each other automatically, as well as Vehicle-to-Grid (V2G) energy transfer — will become mandatory for both public and private charging stations.

Moreover, AFIR is no longer merely a technical standard. It is now directly linked to the EU Cyber Resilience Act (CRA) and the NIS2 Directive. In other words, charging station manufacturers and operators are, for the first time, facing cybersecurity obligations applicable across the European Union. This officially confirms that charging infrastructure is now being treated as part of critical energy infrastructure.

In short, the competition in Europe is no longer about who can install the largest number of charging stations.

The new race is this:

Who can build the smartest, strongest, and most secure charging network?

A modern DC fast charging station is no longer simply an electrical outlet. It is a digital system continuously exchanging data with vehicles, payment systems, mobile applications, energy management software, and the electricity grid itself.

In other words, next-generation charging infrastructure is evolving into a cyber-physical network embedded within the energy sector.

Naturally, this development also creates new risks. European research indicates that cybersecurity vulnerabilities within charging networks may be far more serious than previously assumed. A potential cyberattack may not only disrupt payment systems but could directly affect the balance of electricity distribution itself.

When viewed from this perspective, the 2026 EPDK regulations in Türkiye demonstrate how critical cybersecurity and data management standards have become for charging network operators.

Over the next few years, Türkiye is expected to experience a sharp increase in electric vehicle adoption, targeting between 1 and 1.5 million EVs by 2030, alongside the electrification of heavy commercial transportation and the wider deployment of ultra-fast DC charging stations. When these three developments converge, the issue will no longer be “finding a charging station.” The discussion will instead focus on how the electricity grid will manage this growing demand.

The EPDK regulation published in the Official Gazette in March 2026 sends an important signal in this regard: charging infrastructure is no longer limited to highways and public stations but is also expanding into residential complexes and apartment parking facilities. By 2030, the majority of charging activities are expected to take place within living spaces. This represents a fundamental shift in the market structure and competitive dynamics of the sector.

Megawatt-level charging hubs along logistics corridors will increasingly resemble small energy management centers rather than traditional fuel stations. Energy storage, smart grid management, renewable energy integration, and data security are no longer “additional features”; they are becoming the infrastructure itself.

Competition among players such as Trugo, ZES, Eşarj, Voltrun, and Wat Mobilite is increasingly being shaped on this basis. According to EPDK March 2026 data, Trugo currently leads the market in electricity consumption. TOGG’s investment in Trugo and its cooperation with Shell Recharge are among the first indications that Türkiye is seeking to establish not merely an automotive industry, but a complete charging ecosystem.

Energy management, software infrastructure, data security, and infrastructure planning are now becoming just as decisive as motor technology itself. The sector is expected to exceed a market size of 30 billion TRY by 2030.

As the industry fair approaches, perhaps the most critical question this year will be this:

What is truly shaping the electric vehicle revolution — the vehicles themselves, or the invisible energy infrastructure behind them?

The industry has entered its second act.

And this act will be driven not by automobiles, but by the power of infrastructure itself.

References :

Energy Market Regulatory Authority (EPDK), Charging Service Market Monthly Statistics Report, February 2026. Available at: https://www.epdk.gov.tr (accessed 10 May 2026).

Energy Market Regulatory Authority (EPDK), Charging Service Market Monthly Statistics Report, March 2026. Available at: https://www.epdk.gov.tr (accessed 10 May 2026).

Amendment to the Regulation on Electric Vehicle Charging Services, Official Gazette, 23 March 2026.

European Commission, Commission Implementing Regulation (EU) 2025/655, 18 June 2025. Available at: https://eur-lex.europa.eu (accessed 12 May 2026).

European Parliament and Council, Regulation (EU) 2023/1804 on the Deployment of Alternative Fuels Infrastructure (AFIR), 13 September 2023. Available at: https://eur-lex.europa.eu (accessed 12 May 2026).

“Türkiye’de Elektrikli Araç Sayısı 400 Bini Aştı” [The Number of Electric Vehicles in Türkiye Exceeded 400,000], May 2026. Available at: https://www.enerjiekonomisi.com (accessed 15 May 2026).

“Elektrikli araç şarjında tüketimin üçte biri İstanbul’dan: Soket sayısı 42 bine yaklaştı” [One-Third of Electric Vehicle Charging Consumption Comes from Istanbul: Number of Charging Sockets Approaches 42,000], April 2026. Available at: https://www.donanimhaber.com (accessed 15 May 2026).

“AFIR & EN-ISO-15118: New Obligation for AC Charging Stations from 2026,” June 2025. Available at: https://www.bender.de (accessed 15 May 2026).