You start your day with an email from your customer in Europe. The product you are exporting is the same, the quality is the same… but this time the question is different: “Could you please provide information regarding the carbon footprint of your product?” If you do not have a clear answer to this question, you may no longer be losing just a customer, but an entire market. Because as of 2026, carbon has become a new cost item — invisible perhaps, but directly reflected on invoices.

For many years, the concept of carbon footprint remained buried within the pages of sustainability reports. Companies talked about it, investors read about it, and environmentally conscious individuals and businesses supported it wholeheartedly. Yet until recently, it rarely had a direct impact on everyday commercial decisions. Today, however, carbon is measured, priced, and capable of determining competitiveness just like energy, labor, or raw materials. In some sectors, it has even become more critical than the product itself. In Europe, some importers now prefer purchasing the same product at a higher price simply because it has a lower carbon footprint. The real cost is no longer merely the product price, but the carbon burden carried by that product.

By the end of 2025, Türkiye had also begun to feel the effects of this transformation. Due to its strong trade relations with the European Union, Türkiye is among the countries most rapidly affected by this shift. For exporters in sectors such as iron and steel, cement, and aluminum, carbon is no longer a theoretical concept but a direct “entry ticket” to the market. While the foundations of a carbon market are being laid through the Turkish Climate Law, emissions measurement and reporting practices are rapidly becoming widespread among companies. Yet a critical turning point exists here: in Türkiye, merely measuring carbon is no longer sufficient. What matters now is managing and reducing emissions properly. Europe is no longer asking only “How much carbon do you emit?” It is also purchasing the answer to the question: “How much are you reducing it?”

The transition period implemented between 2023 and 2025 was perhaps underestimated by many. Reports were submitted and systems were established, yet most companies did not fully realize that this process would evolve into a real financial burden. In 2026, several new provisions and practices directly affecting companies were introduced under the CBAM (Carbon Border Adjustment Mechanism) legislation. As of 1 January 2026, CBAM moved beyond the transitional reporting phase and entered the stage of binding financial obligations. This means that importers are now required to purchase carbon certificates.

Paper-based reporting has ended. Importers must digitally report all imports of goods falling within the CBAM scope to the European Commission. Data provided by customs authorities is automatically transferred to the Commission. In the first phase, iron and steel, cement, aluminum, fertilizers, electricity, and hydrogen products were definitively included within the regime. Naturally, sectors indirectly affected — such as the automotive supply industry — have also begun conducting risk analyses.

Companies are now required to ensure that their declared emissions data is verifiable and auditable. This makes independent verification procedures mandatory. With the secondary legislation package published by the European Commission on 17 December 2025, the framework of the financial obligations to be applied as of 2026 was clarified. Importers bringing in less than 50 tons annually are, for the time being, exempt from CBAM obligations. It should also be noted that declarations relating to the year 2026 must be submitted no later than 30 September 2027.

The steps required for compliance are quite clear. Companies must measure carbon emissions arising from their production processes and have these data verified by independent verification bodies. Transitioning to digital reporting systems requires the establishment of infrastructure compatible with customs declarations and capable of providing regular and accurate data transfers to the EU CBAM platform.

For products exported to the EU, the obligation to purchase carbon certificates will apply, and consequently, certificate costs will need to be reflected in pricing structures and contractual arrangements.

The legal dimension of the matter is equally important. Carbon costs must be clearly regulated in contracts concluded with EU buyers, while compliance with both CBAM and the CSRD (Corporate Sustainability Reporting Directive) must be taken into account. Preparing Product Carbon Footprint (PCF) and Environmental Product Declaration (EPD) documentation, as well as entering into renewable energy procurement agreements (RE-PPA), will become increasingly essential in order to achieve a low-carbon production advantage.

Türkiye will also continue monitoring its transition process toward its own Emissions Trading System (ETS), attempting to balance local carbon pricing mechanisms with EU CBAM obligations. Consequently, companies seeking compliance with CBAM 2026 must simultaneously manage both technical processes (emissions measurement and reporting) and commercial processes (contractual adaptation and cost management). Companies that prepare early may gain a significant competitive advantage within the EU market.

Today, for carbon-intensive products exported to Europe, merely providing data is no longer sufficient. A real financial cost is now attached to every ton of carbon emitted. This cost is determined according to prices within the European carbon market and often directly affects product profit margins.

One of the most striking developments in this regard is the emergence of the “authorized declarant system.” In order to export to Europe, companies must now be approved not only for their products, but also in terms of their carbon performance. Trade is therefore evolving from a technical issue into a form of “carbon passport” system.

Moreover, if a Turkish company already pays a carbon price domestically, that cost may be deducted within the European system. This mechanism clearly demonstrates why establishing Türkiye’s own carbon market is not merely an environmental matter, but also a strategic economic decision.

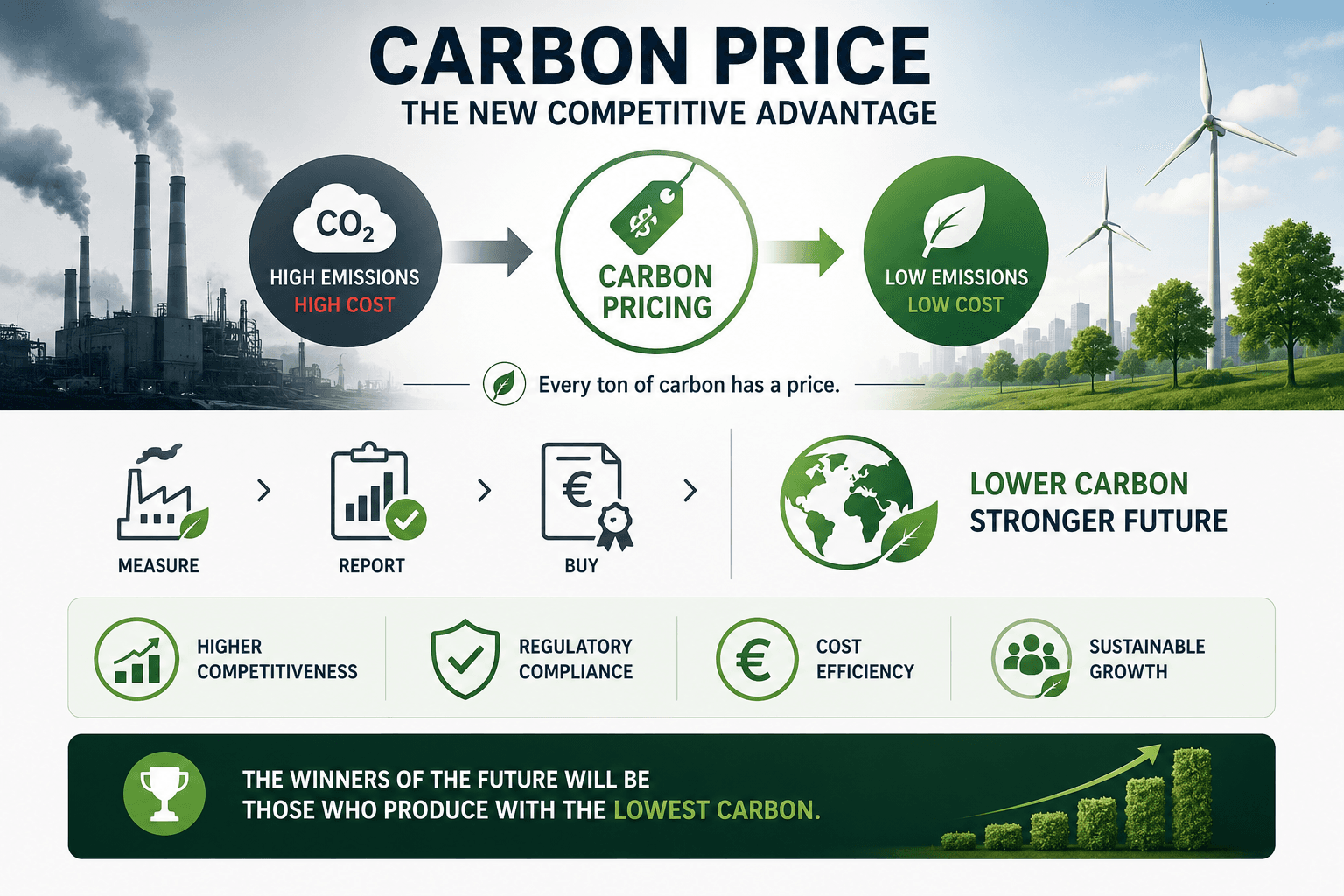

Globally, carbon is increasingly behaving like a common currency. Although Europe pioneered this system, many countries — from China to the United States — are developing their own carbon pricing mechanisms. This creates an interesting paradox: countries that once benefited from low-cost production may now become disadvantaged due to carbon costs. Low-cost production alone is no longer enough. Low-carbon production is the new competitive advantage.

At first glance, this transformation may appear threatening. Rising costs, new regulations, and technical requirements can undoubtedly be challenging for many companies. Yet on closer examination, this process also presents a major opportunity. Companies investing in energy efficiency, transforming their production processes, and actively managing their carbon emissions are entering a new competitive arena. Such companies not only reduce their costs but also gain access to higher-value markets.

Many European companies now evaluate suppliers not only based on price, but also on carbon performance. In some cases, carbon performance has even begun to outweigh pricing considerations.

In summary, as of 2026, carbon is no longer a figure hidden in the footnotes of sustainability reports. It has become an invisible balance-sheet item determining the true value of companies. Because today, the price of a product is shaped not only by its production cost, but also by the trace it leaves in the atmosphere.

For Türkiye, this process represents far more than a simple compliance issue. It is a decision about whether or not to remain part of global competition. And perhaps the most striking reality is this: in the future, the winning companies will not be those producing at the lowest cost, but those producing with the lowest carbon emissions.